A garnishee notice is a notice issued by the Australian Taxation Office (“the ATO”) to a third-party of a tax debtor, directing any monies held on behalf of the tax debtor be transferred to them.

A garnishee notice is a notice issued by the Australian Taxation Office (“the ATO”) to a third-party of a tax debtor, directing any monies held on behalf of the tax debtor be transferred to them.

ATO garnishee notices can very often be embarrassing to the taxpayer and can sometimes damage the business as it can force third parties into the business’s financial issues.

This garnishee notice may also cause significant cashflow issues for the business.

The ATO can send a garnishee notice to a number of different third parties. For individual tax debtors, the ATO can possibly send a garnishee notice to:

- A person who owes the tax debtor money from the sale of real property.

- The tax debtor’s employer or head contractor.

- The tax debtor’s financial institutions including banks and building societies.

For business tax debtor’s, the ATO can possibly send a garnishee notice to:

- The tax debtor’s business financial institution, bank, or building society.

- The tax debtor’s business suppliers of merchant card facilities.

- The tax debtor’s business trade debtors.

In this article, our Queensland tax debt lawyers explain the basics of resolving tax debt disputes with the ATO.

If an ATO garnishee notice has been issued, then contact our litigation and dispute resolution lawyers to discuss

CONTACT A LITIGATION LAWYER TODAY

OR CALL: 1300 545 133 FOR A FREE PHONE CONSULTATION

What is a garnishee notice?

As above, a garnishee notice is a tool used by the ATO to recover tax debts from a tax debtor.

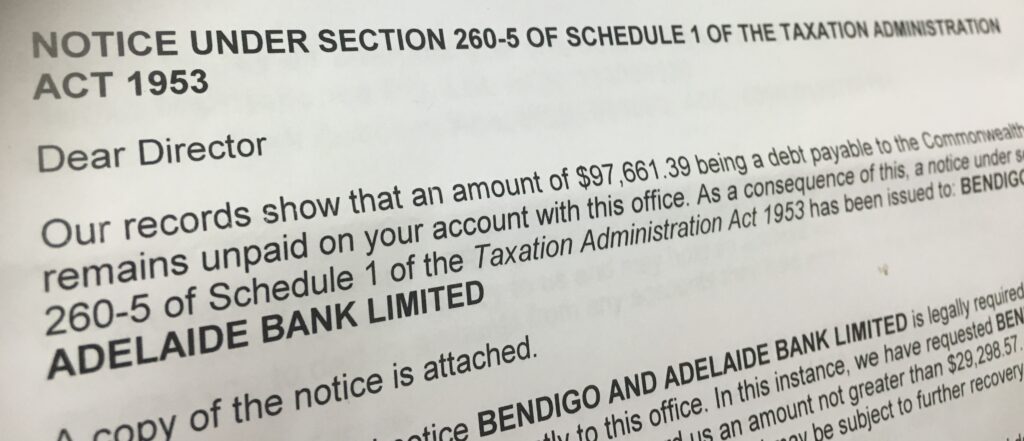

The authority is given to the ATO by section 260-5 of schedule 1 of the TAA. Section 260-5(1) says:

(1) This Subdivision applies if any of the following amounts (the debt) is payable to the Commonwealth by an entity (the debtor) (whether or not the debt has become due and payable):

(a) an amount of a * tax-related liability;

(b) a judgment debt for a * tax-related liability;

(c) costs for such a judgment debt;

(d) an amount that a court has ordered the debtor to pay to the Commissioner following the debtor’s conviction for an offence against a * taxation law.

So, garnishee notice can be issued for:

- A tax debt; and/or

- A judgment given on a tax debt; and/or

- The ATO’s costs of obtaining judgment on a tax debt.

Section 260-5(2) of the TAA then goes on to say:

The Commissioner may give a written notice to an entity (the third party) under this section if the third party owes or may later owe money to the debtor.

This section of the TAA authorises the ATO to serve a written garnishee notice on any third party, if that third party owed money to the tax debtor.

Section 260-5(3) of the TAA then goes on to say:

(3) The third party is taken to owe money (the available money) to the debtor if the third party:

(a) is an entity by whom the money is due or accruing to the debtor; or

(b) holds the money for or on account of the debtor; or

(c) holds the money on account of some other entity for payment to the debtor; or

(d) has authority from some other entity to pay the money to the debtor.

The third party is so taken to owe the money to the debtor even if:

(e) the money is not due, or is not so held, or payable under the authority, unless a condition is fulfilled; and

(f) the condition has not been fulfilled.

The ATO garnishee notice will require the third party to pay the alleged amount of the tax debt immediately after issuance; or within a specified time after the amount of the available money concerned becomes an amount owing to the debtor.

These two types of garnishee notices are called:

- Point in time notices; and

- Continuing notices.

We will explain the difference in more detail below.

Have you been issued with a director penalty notice? Read our director penalty notice article here.

Point in Time ATO Garnishee Notice

Point in time notices are notices which demand a single one-off payment.

For example, the tax debtor’s bank must pay the full tax debt, or a certain percentage, from the specified account of the tax debtor, whichever is less.

This is given authority by 260-5(4)(a) of the TAA which says:

(4) A notice under this section must:

(a) require the third party to pay to the Commissioner the lesser of, or a specified amount not exceeding the lesser of:

(i) the debt; or

(ii) the available money

Section 260-5(4)(a) of schedule 1 of the TAA authorises the single payment from the third party of the tax debtor.

There are also continuing garnishee notices.

Continuing ATO Garnishee Notice

Continuing notices are notices which demand continuous payments from the third party.

For example, the tax debtor’s bank must pay an amount of money in the bank account, as well as any future deposits.

This is given authority by 260-5(4)(b) of schedule 1 of the TAA which says:

(4) A notice under this section must:

(b) if there will be amounts of the available money from time to time–require the third party to pay to the Commissioner a specified amount, or a specified percentage, of each amount of the available money, until the debt is satisfied.

Section 260-5(4)(b) authorises the continuing payments from the third party of the tax debtor.

As you can see, the ATO’s legal power to issue a garnishee notice are powers given to the ATO pursuant to section 260-5 of schedule 1 of the Taxation Administration Act 1953 (Cth).

The ATO may issue a garnishee notice to various third parties.

What is the Third Party Required to Do?

When issued with a garnishee notice, the third party has a certain time frame to comply with the notice.

The third party must comply with the garnishee notice, or they face serious penalties. If they do comply then it is deemed to have been made with the tax debtor’s consent.

If the third-party does not comply with the garnishee notice, then this is a criminal offence. The penalty for non-payment by the third party are:

- A fine (20 penalty units); and

- Liability to pay the amount of the garnishee notice.

As you can see, the conditions are onerous for the third party, and they must pay of face the punishment above. If you are unsure then it is vital you get advice from a tax dispute lawyer.

Who Can the ATO Issue Garnishee Notices To?

The ATO can issue a garnishee notice to the following:

- A contractor who owes money to a tax debtor, and other trade debtors.

- An employer who owes money to a tax debtor.

- Banks, financial institutions and building societies where the tax debtor has accounts.

- People involved in the sale of land or property from a tax debtor such as purchasers, real estate agents and solicitors.

- Solicitors or accountants holding funds in trust on behalf of a tax debtor.

- An Australian company in which a tax debtor is a shareholder; and

- The suppliers of merchant card facilities.

The ATO’s reach is long, and the issuance of a garnishee notice on any one of these may cause devastating and long-lasting damage to the taxpayer’s business and business relationships.

It is very important that you seek advice as soon as you receive a garnishee notice.

Why have the ATO Issued a Garnishee Notice?

Why has a garnishee notice been issued? A garnishee notice will be issued by the ATO against the tax debtor in the following circumstances:

- The tax debtor does not pay a tax obligation and fails to take reasonable steps with the ATO to resolve this dispute.

- The tax debtor has repeatedly defaulted on it agreed ATO taxation payment plans.

- The tax debtor has shown that they are not willing to work with the ATO to resolve the dispute.

- The tax debtor seems to be engaging in illegal phoenix activities.

- The tax department has detected deliberate and ongoing avoidance in relation to an ATO tax audit.

Basically, don’t stick your head in the sand! If you owe tax to the ATO, just work with them to organise repayments.

What does the ATO Consider when Issuing Garnishee Notices?

The ATO will consider a number of things when deciding whether to issue a garnishee notice.

These will include (inter alia) the tax debtor’s financial position, and whether the tax debtor will be at risk of providing for their family, or business.

The ATO Practice Statement Law Administration 2011/18 says at 108:

The ATO will consider the following when deciding whether to issue a garnishee notice:

- the likely implications on the tax debtor’s ability to provide for a family or maintain the viability of a business should the notice be issued.

- the tax debtor’s financial position and circumstances and the steps the tax debtor has taken to pay the debt in the shortest possible time frame;

- whether the revenue is placed at risk because of the tax debtor’s actions (ie paying other creditors in preference to the ATO); and

- any other debts that the tax debtor owes.

So, the ATO should avail itself of the information required above before it was to issue a garnishee notice. If one is issued, are there any defences to an ATO garnishee notice?

Defences to an ATO Garnishee Notice

There are several things that a tax debtor can do to try to stop the third party from making the payment to the ATO. These include:

- Confirming that all of the formal requirements of the garnishee notice are included.

- If the garnishee notice is issued on a judgment, check if there is a stay of enforcement of the judgment, or appeal available to the tax debtor.

- If the funds are held in a self-managed superannuation fund account, held in a joint account, or held in foreign currency.

- If the garnishee notice has been issued by the ATO for an improper purpose or in bad faith.

However, these defences are not strong defences and are risky applications to make and be successful.

It is always good to check with your tax debts lawyer.

You could also try mitigating the deductions the third party has to pay by:

- If the garnishee notice is against your employer, you can resign.

- If the garnishee notice is against your bank, you can change banks.

Alternatively, the underlying tax assessment the ATO has sent may also be challenged in Court proceedings. The Federal Court has jurisdiction to review tax assessments.

Defending tax debts can be difficult because of the general rule that a tax assessment is conclusive evidence:

- Of the amount of tax payable, interest owing and penalties; and

- That the taxation itself assessment was properly made by the ATO.

This means that the taxpayer may still have to pay the entire assessed amount to the ATO, even if there is a genuine dispute about part of the tax liability.

If you get a notice that the objection to the tax assessment was not successful, and you file an appeal in the AAT or the Court, then you may still be required to pay the entire amount of the tax assessment.

Because of this, it can be very difficult to defend tax debt proceedings in Court.

However, the ATO may agree to withdraw garnishee notices.

Will the ATO agree to Withdraw the ATO Garnishee Notice?

The ATO may agree to withdraw or amend a garnishee notice in certain situations.

The ATO Practice Statement Law Administration 2011/18 says at 109 states:

The Commissioner will consider any reasonable request from a tax debtor to either withdraw or vary the requirements of a garnishee notice, provided the tax debtor makes suitable alternative arrangements for payment.

If the ATO can see that a tax debtor is actually trying to resolve their tax debts, they may agree to withdraw the garnishee notice.

This will usually mean that the tax debtor is prepared to enter into a payment plan for the payment of the tax debt.

What is an ATO Payment Plan?

An ATO payment plan is an agreement between the tax debtor and the tax office which allows the tax debtor to pay the outstanding tax in instalments.

There are usually some conditions attached, such as being up to date with all other tax obligations, and/or the plan being for no longer that 12 months.

If the tax debtor and the ATO agrees to the payment plan, then the ATO may withdraw the garnishee notice.

A garnishee notice will usually have a person of contact at the ATO. If you want to arrange a payment it is vital that you contact that person, or the ATO, before the third party is required to make the payment.

An experienced negotiator may also be able to reduce your tax debt liability by negotiating for the reduction of the added interest and penalties.

What Type of Payment Plan Should I Enter?

There are a number of different payment plans that a tax debtor can enter into, based on the circumstances of your particular situation.

Some ATO payment plans may last for three (3) months, and some ATO payment plans may last for over two (2) years, or more. Most are for up to 12 months.

Some ATO payment plans may require an upfront payment before making monthly repayments, and some ATO payment plans may not require any upfront payments.

The type of payment arrangement that a tax debtor can negotiate with the ATO depends on several different factors, such as:

- The amount of the debt owed to the ATO.

- The amount of money a tax debtor can afford to pay.

- Whether the tax debtor is able to provide security to the ATO (mortgage, for example); and

- The tax debtor’s compliance history with the ATO.

The best way to mitigate risk, is to avoid being given a garnishee notice in the first place.

How to Avoid Being Issued with a Garnishee Notice?

I realise that if you are reading this on our website, you or your client has likely already been served with an ATO garnishee notice.

However, there are a number of things that a taxpayer can do to avoid any ATO adverse action:

- Do not ignore the warnings from the ATO.

- Act quickly to get the alleged tax debt resolved.

- Negotiate a payment plan with the ATO.

- If you cannot pay, then appoint a liquidator or bankruptcy trustee.

- Get professional accounting and legal advice.

The best advice is not burying your head in the sand.

If the ATO claim you have a tax liability, then you should attempt to do something. Do not just do nothing and hope you get some more money in the future.

The ATO is a Secured Creditor Because of the Garnishee Notice

Care should be taken with ATO garnishee notices because once issued, the ATO becomes a secured creditor by way of a statutory charge over the monies held by the third party.

In Hansen Yuncken Pty Ltd v. Ian James Ericson trading as Flea’s Concreting & Anor [2012] QSC 51, McMurdo J said at [35]:

It must be accepted then that the service of a s 260-5 notice confers upon the Commissioner what has been described as a statutory charge over the relevant debt. But that is not sufficient to dispose of the present contest, because it is a charge in a limited sense and, in particular, it is not a charge which provides the Commissioner with a proprietary interest in the subject debt.

Again, this gives the ATO advantages, so if it can be withdraw then the tax debtor will be in a better position.

Conclusion on ATO Garnishee Notices

If a third party has been served with a garnishee notice, then the tax debtor must act quickly to avoid that debt being paid.

The tax debtor can take some steps to defend the garnishee notice, but the defences are usually very difficult to be successful.

A tax debtor may be able negotiate a payment plan in exchange for the garnishee being withdrawn.

Most importantly, act quickly and get qualified legal advice as soon as possible.

If an ATO garnishee notice has been issued, then contact our litigation and dispute resolution lawyers to discuss

CONTACT A LITIGATION LAWYER TODAY

OR CALL: 1300 545 133 FOR A FREE PHONE CONSULTATION

Garnishee Notice Frequently Asked Questions FAQ

We get asked questions in relation to garnishee notices. We have selected a few of the most commonly asked questions below.

How much can the ATO garnishee?

The entire amount of the overdue tax assessment can be collected. However, the ATO will not take more that 30% of any wages or salaries garnished.

How do I know if a notice has been sent by the ATO?

If the ATO sends a garnishee notice to a third party, they are also obliged to send a copy to the tax debtor. Section 260-5(6) of schedule 1 of the Tax Administration Act says, “The Commissioner must send a copy of the notice to the debtor”.

What should I do if I receive a notice?

If you are a third party, then you must pay the amount requested before the expiration of the payment period, or you may get a fine or be liable for the debt.

If you are a tax debtor then you must act quickly, and you may be able to get the garnishee notice withdrawn in exchange for a payment plan.

When can the ATO issue a garnishee notice?

If there is a tax debt liability, and the tax debtor has:

- Failed to take reasonable steps to resolve this; or

- Repeated defaults on payment plans; or

- Unwillingness to work with the ATO; or

- Illegal phoenix activity; or

- Deliberate and ongoing avoidance.

Can the ATO issue a garnishee notice if the company is in external administration?

The ATO cannot issue a garnishee notice once the company is in liquidation (Bell Group Limited (in liq) v DCT [2015] FCA 1056).

The third party may still be liable if the garnishee notice was issued prior to the company going into liquidation.

However, the Garnishee Notice creates a statutory charge over the monies held by the third party to the ATO, making the ATO a secured creditor.

Who receives a garnishee notice?

Both the tax debtor and the third party will receive the notice.

The third parties include a contractor, employer, banks, financial institutions and building societies, purchasers of real property, real estate agents, solicitors, accountants, a company in which a tax debtor is a shareholder; and suppliers of merchant card facilities.

What happens after I receive a notice?

If you are a third party, you must pay the amount contained in the ATO garnishee notice.

If you are the tax debtor, you must attempt to either defend the garnishee notice on technical grounds or negotiate a payment plan with the ATO in exchange for it to be withdrawn.

How can I challenge a garnishee notice?

You can challenge the garnishee notice on the following grounds:

- Ensuring that all of the formal requirements of the garnishee notice are included; or

- Obtain a stay of enforcement of the judgment debt; or

- Ensure the funds are not held in a joint account or held in foreign currency; or

- Check if notice has been issued for an improper purpose or in bad faith.

If an ATO garnishee notice has been issued, then contact our litigation and dispute resolution lawyers to discuss

CONTACT A LITIGATION LAWYER TODAY

OR CALL: 1300 545 133 FOR A FREE PHONE CONSULTATION